Those who are still arguing whether Kalshi or Polymarket will dominate the prediction market landscape are missing the big picture. Prediction markets are becoming real infrastructure, and the eventual winners will be decided by who can occupy key product archetypes as the stack stratifies, not a winner-takes-all landslide.

That stratification is already visible. On one end, crypto-native rails like Polymarket optimize for breadth, speed-to-list, and narrative relevance; on the other, regulated rails like Kalshi optimize for settlement credibility and distribution compatibility. But the real accelerant is happening one layer up: execution wrappers like Coinbase and Robinhood are turning event contracts into a mainstream instrument shelf, while TradFi incumbents like Nasdaq and Cboe are pushing standardized, hedging-grade binaries that fit neatly into existing market structure and compliance regimes.

This report gives you the framework to understand where the category is headed, not as a binary “onchain vs offchain” debate, but as a stack war between rails and wrappers that productize into repeatable archetypes. We’ll map the market into the product formats users actually adopt, show where liquidity is truly tradeable (and where it breaks), explain how “probability-as-data” is becoming a parallel business line, and close with our base, bull, and bear cases for the sector.

The prediction market sector in 60 seconds

What was dismissed as a passing trend around the 2024 election cycle has ballooned into a class of derivatives that does billions of dollars of volume every week.

Polymarket and Kalshi are trading blows in the standings of volume, depth, and breadth. Overall, the sector is thriving. In the beginning of 2024, you could sneeze and slip the price of every market by 10 cents, but by the fourth quarter of 2025, Polymarket and Kalshi had thousands of markets that could absorb a $10K trade within 1¢ of price impact.

This diversification can be visualized through the Herfindahl-Hirschman Index (HHI), which can tell us when an ecosystem becomes overreliant on too few market leaders.

We see that, for all of the worry, the end of the 2024 election season represented only a momentary high point in the concentration of prediction market activity.

Each bar represents a market category (e.g. “US Election,” “Crypto Prices,” “Sports”) - not a platform. HHI = Σ(share²). Drag bars to simulate how volume concentration across market categories affects ecosystem health. Under 1,500 = competitive. Over 2,500 = highly concentrated.

Drag bars up/down to adjust market share

Prediction market sector deep dive

The important thing to re-learn is that these are not all one product. Prediction markets are simultaneously:

- A trading venue, with execution, spreads, and risk transfer,

- A media/data product, that people cite and lean on for headlines,

- A hedging platform, where traders can de-risk unique tail risks,

- And a decision-support tool or a way to derive signal via market incentives

This category has been so hard to analyze because people argue “gambling vs forecasting,” but that’s the wrong axis. The right question to ask is which user intent you’re serving, and how that maps onto distribution, liquidity, and settlement.

User Archetypes

Speaking of users, prediction markets have to be specific about who their target market is and, more importantly, who it is not. People come to use these platforms for many reasons, but here are some of the usual participants:

Information traders: These users attempt to locate market mispricing and capitalize. They need tight spreads, reliable settlement, and prefer low fees. You could throw “information-advantaged” (both legitimate and not) traders in here too, which we can explore later.

Narrative commentators: These folks express and contest narratives in real time and generally focus on crypto & politics. They value a wide breadth of available markets to be hyper-specific about their views and don’t necessarily need super deep liquidity.

Gamblers: Value a comfortable balance of market depth and breadth, with an overweighting towards sports markets and a propensity for combo bets/parlays and social attention loops.

Hedgers: Generally prefer to trade markets with clear financial/economic exposure (macro releases, policy outcomes, rate decisions) and value deep liquidity and very clear resolution criteria.

Bots/agents: Kind of a wildcard to think through, but agents are OK with placing tiny trade amounts and racking up miniscule gains, but they need clean tool access and prefer low fees.

Once the platform has located its target audience, it can begin optimizing for what they truly value in a prediction market.

Rails vs Wrappers and how to map products to users

From the platform perspective, we find it helpful to shape a mental model around two layers of the stack:

Rails = where liquidity, execution, and settlement live.

Wrappers = where distribution, UX loops, and packaging live.

The team that owns the distribution does not necessarily have to own the base-layer liquidity. There can be stack competition between: who owns the rails, who owns the wrapper, and who can think up clever combinations between the two that serve a target audience.

In practice, we see this manifest in several distinct “product archetypes.” Here’s how it breaks down.

| Type | Priority | Key Features | Best For | Drawbacks | Example(s) |

|---|---|---|---|---|---|

| Narrative Markets | Attention-first | Bespoke (often permissionless) market creation | Narrative Participants, (some) Information Traders | Worst for Hedgers (too much semantic risk) | Polymarket |

| Cadence Markets | Retention-first | Combos/parlays, attention feedback loops | Gamblers (especially sports), casual / mobile users | Needs RFQ/quoting mechanics, can lack depth vs. breadth | Robinhood, Kalshi, Coinbase |

| Hedging Markets | Verification-first | Deep liquidity for a smaller set of markets, focused on econ/finance | Hedgers, Institutions, (some) Information Traders | Narrower catalog, slower listing, higher spec rigor | CME, Nasdaq/Cboe(?), Hyperliquid HIP-4 |

Narrative markets such as Polymarket (could also add in Opinion, Limitless, XO Markets, etc.) benefit from the ability to have high specificity in their markets. They are able to take the topics that everyone is chatting about around the watercooler (or, let’s face it, on X) and turn them into real-deal betting markets. Their edge is their ability to capture attention and headlines, the speed-to-list new markets, and their de facto position as offering “odds” as a form of media.

The obvious risk of a fast-and-loose market generation philosophy is that resolution disputes are inevitable. When money is on the line and the rules are even a little vague, there will be disagreements. And even if they are trending down against adoption (now just 4 disputes per 10,000 markets), the edge cases make the news and frustrate users.

Cadence Markets leverage the dopamine spikes caused by consistent feedback loops involved in high-cadence markets, with sports betting being the number one vertical. These businesses can be extremely profitable, and they’re able to charge higher fees as sportsbetters will generally accept a higher percentage fee compared to, say, an investor or arbitrageur. Venues like Kalshi and Robinhood have begun implementing parlays/combo bets, which ratchet up the profitability of the platforms.

Robinhood and Coinbase are actually very interesting case studies of the Rail vs. Wrapper distinction, with both exchanges using Kalshi to solve their cold-start problem during the initial spin up phase. Robinhood has since added their own markets (capturing the Rail business) and Coinbase plans on integrating “contracts from additional prediction market platforms in the coming months” (establishing themselves as the Wrapper of all Wrappers).

Spinning up these combo bets can be difficult from a practical and a regulatory point of view. Practically, establishing a RFQ (Request for Quote, where these multi-leg custom bets are offered to many market makers to see who can quote the best price) is more technically difficult than a simple orderbook and tends to fracture liquidity into many small and bespoke buckets instead of keeping dollars in a single book. On top of that, sports betting is already top-of-mind in the eye of regulators, especially at the state level. And by slapping an RFQ system in the mix, this might start to look (to some) more like a dealer-packaged derivative than a simple CLOB matching. (Late breaking: CFTC rules around these may be easing!)

Hedging Markets are what we perceive to be around the corner. Institutional giants Cboe and Nasdaq are joining in on the party, looking to roll out prediction market options in the near future. We see the focus of this subset to surround real financial exposure (macro releases, policy outcomes, and rate decisions to name a few) so sophisticated investors can specify exact risks they would like to hedge out. Note that CME has been early, but they’re off partying with DraftKings and FanDuel, with a larger focus on retail/sportsbetting at the moment.

Hedging markets will require dead-simple resolution criteria and standardized market creation. These guys aren’t gonna mess around with Zelensky’s suit, they’ll have markets like “Will Crude Oil futures be above or below $90.00 at 4PM ET on March 6th, 2026?”. These are for risk transfer, not for entertainment. Not very fun, but useful to the poor sap trading airline stocks.

Polymarket vs Kalshi

Speaking of the two titans, let’s address the elephant in the room. But I want to be clear up front, this isn’t about “who wins”; both can be right at the same time because they’re optimizing different parts of the stack and different product archetypes.

It all comes down to: where does price discovery take place, and what kind of user-product bundles does each rail naturally produce?

The pair’s differences started at the very beginning, with Polymarket setting up an onchain architecture on Polygon and pursuing a later-stage compliance path, while Kalshi built entirely offchain and went down the regulation path before selectively exploring onchain components.

This resembles the perps “engine vs settlement” split: where is matching performed, where is settlement finalized, and how do you anchor your trust? With perp DEXs, this winning architecture seems to be either - a) an entirely off-chain orderbook + onchain settlement or verification OR b) a high-performant (and mostly centralized) onchain orderbook. It remains to be seen whether Kalshi or Polymarket will arrive at a hybrid conclusion such as this, but I’d argue that their final form is yet to be revealed.

Polymarket is optimizing for long-tail execution scaling with permissionless market generation to cater to whatever their users want to bet on. This hyperspecificity uniquely positions them as the “place to trade narratives” and basically becomes the likelihood extension of the topic du jour, turning attention into a public probability surface.

This positions them as a “probability” brand, and a plausible path is that they continue to parlay this positioning into data partnerships with news organizations and trading venues.

Their vibe-check-as-a-service architecture means they no longer solely have to rely on trading fees to meet their bottom line. In other words, they become a “truth API” and organizations pay to get a direct feed.

At the beginning of 2025, Kalshi made the decision to push heavily into sports. Part of this is likely just product physics: after the 2024 election cycle, the category’s “always-on” attention moved away from politics, and sports is the highest-frequency substrate available - there’s always another match, another slate, another moment to trade.

This pivot is also the cleanest expression of what we call Cadence Markets: a subset of prediction markets optimized for high feedback loops and habitual usage. In Cadence Markets, the product goal isn’t “the world’s most philosophically pure probability estimate” - it’s getting users to return, wager, and repeat. That changes everything about what you build and what you can monetize.

Combos (parlay-like packaging) are the retention superweapon here. They let users express richer views, feel like “builders” rather than simple bettors, and keep them engaged across a calendar of events instead of a handful of headline markets.

But combos also force a structural reality: you need someone willing to quote the bundle. In practice, that pushes you toward RFQ-style mechanics and tighter risk management, because you’re no longer just matching two-sided flow in a single contract - you’re packaging legs into a single exposure that must be priced and warehoused, at least temporarily.

The distribution strategy fits the archetype. Retail sports flow is far more UX-sensitive than fee-sensitive - most users only care about frictionless onboarding, fast feedback, and the ability to close positions easily. That’s precisely why Kalshi’s partnerships with brokers/wrappers (like Coinbase and Robinhood) matter: a large distribution surface concentrates flow, concentrated flow tightens execution, tighter execution improves retention, and better retention attracts more liquidity provision. That flywheel is hard to replicate if you’re not plugged into where users already trade.

The takeaway is that we’re witnessing specialization - we’re watching rails and wrappers recombine into different product archetypes. Kalshi’s cadence-first path is one extreme; Polymarket’s narrative-first path is the other. The next section goes deeper: we have the current frontrunning rails, but where does the rest of the ecosystem stand?

How much would your trade actually cost? Pick a platform, trade size, and market tier to estimate your all-in execution costs.

Based on real data from S6-14, S6-07, and S6-06 across 476M trades.

⚠ These execution costs reflect spread and displacement only - they do not include platform trading fees. With Polymarket’s new fee structure (effective March 30, 2026), actual all-in costs will be higher. Kalshi has charged fees since inception; Polymarket’s historical data was largely fee-free.

Where the money is actually being made

With both leaders’ private valuations pushing into the 11 figures, they have to show a path to profit at some point, so it’s no surprise that Polymarket recently joined Kalshi in charging fees on most markets. But the comparison is not quite apples-to-apples, with each side using their fee structure to signal which users they truly optimize for.

How do effective taker fee rates compare across platforms and market categories? Polymarket’s new fee structure (effective March 30, 2026) introduces category-specific rates with different curve shapes. Kalshi uses a uniform formula with a halved rate for index markets. Click legend items to toggle lines on/off.

The formula rate × P × (1−P) taxes the variance of your payout - maximum at 50/50 (peak uncertainty), zero at the extremes. Your effective rate is rate × (1−P): longshot buyers at 5¢ pay ~6.7%, while near-certainties at 95¢ pay ~0.35%.

The formula feeRate × (P(1−P))exp is symmetric - you pay the same effective rate at 20¢ and 80¢. But the exponent and rate vary by category, letting Polymarket price each market type differently. Geopolitical is free (maximizing the data surface), Politics is cheap, Crypto is expensive.

Kalshi: Retail entertainment flow on longshots pays higher effective rates - subsidizing the platform through volume count.

Polymarket: Sports (0.75% peak) is the cheapest non-free category, designed to attract high-frequency repeat engagement. exp=1

Kalshi: Same formula as everything else - no special treatment for attention-driven flow.

Polymarket: Politics/Finance/Tech at 1.00% peak; Geopolitical is completely free - subsidizing the “probability surface” that powers media embeds and data licensing. exp=1

Kalshi: Institutional hedgers buying at 90¢+ pay <0.7% effective rate - the formula naturally rewards precision risk-transfer. S&P/Nasdaq halved to 0.035.

Polymarket: Economics/Weather use exp=0.5 - a flatter curve that still charges at extreme prices where informed traders operate.

A few things jump out. Polymarket undercuts Kalshi in every single fee-bearing category at every price point up to 90¢. Even Crypto, Polymarket’s most expensive category at a 1.80% peak effective rate, is roughly half of Kalshi’s 3.50% at 50/50 odds. Kalshi only becomes competitive at extreme near-certainties (90¢+), where its effective rate drops below 0.7% - precisely the price range where institutional hedgers operate. That’s not an accident.

Meanwhile, Kalshi’s halved S&P/Nasdaq rate (0.035 vs 0.07) is a targeted concession to win index-derivative flow from TradFi. But even at half rate, it still costs more than Polymarket’s Economics category at every price except 99¢. The message: Kalshi is betting that compliance credibility and settlement enforceability justify the premium, while Polymarket is betting that lower fees plus permissionless market creation will win on volume.

And then there’s Polymarket’s decision to make geopolitical markets completely free - it signals that the real monetization isn’t in trading fees at all, but in the data surface those markets create.

Remember to think in terms of the stack - execution fees are not the only place to charge rent. Often, the largest rents sit at:

Rails - Where execution and settlement live

| Strategy | What they capture | Examples |

|---|---|---|

| Crypto-native execution | Trading fees / take-rate; liquidity network effects; “reference” probability surface | Polymarket - positioned as the “world’s largest prediction market” |

| Regulated execution | Trading fees; settlement enforceability; compliance credibility that enables broker distribution | Kalshi - seeded by Coinbase, Robinhood, and Interactive Brokers |

| TradFi hedging-grade entrants | Standardized, spec-heavy contracts under existing options/clearing regimes | Nasdaq Cboe CME - outcome-related options frameworks |

Wrappers - Where distribution and monetization live

| Strategy | What they capture | Examples |

|---|---|---|

| Retail broker distribution | Order flow + retention loops; cross-sell/wallet share; routing leverage over rails | Coinbase Robinhood - both seeded with Kalshi |

| Consumer gaming distribution | Mobile + high-frequency engagement; same as above, optimized for cadence | FanDuel Predicts - built on CME rails |

| Institutional front-ends | Embedding event contracts into existing macro/risk workflows | Tradeweb ↔ Kalshi partnership |

| Media / publisher embeds | Licensing fees for “probability-as-media” modules | Dow Jones ↔ Polymarket (WSJ/Barron’s/MarketWatch). CNBC ↔ Kalshi |

| Institutional data feeds | Enterprise data distribution; “event-driven data” as a product | ICE ↔ Polymarket: global distribution of event-driven data |

| Analytics terminals | Subscription/lead-gen; flow intelligence (who’s buying/selling) | PredictFolio - portfolio tracking for Polymarket |

| Execution terminals / bots | Power-user UX; advanced orders; cross-venue access | Flipr - cross-platform Polymarket/Kalshi |

| Discovery / aggregation | “Best available” discovery; paired-market comparison | Oddpool MarketPinger - cross-platform search + gap detection |

While rails capture the trading fees, the wrappers have freedom to experiment with financialization. They could charge:

- Attention rent by owning the default location where probabilities are consumed,

- Flow rent by controlling the funnel/routing choices to different rails,

- Cross-sell rent by pushing add-ons to users while leveraging the high-engagement prediction markets,

- Or embed their own custom monetization through strategies like spreads on funding rails, subscriptions, premium tools, or even just plain old ads.

Follow a dollar of trading volume as it flows through the prediction market stack. Hover over any node to highlight its connections.

⚠ Flow sizes are illustrative and represent relative magnitude, not exact dollar amounts. Actual revenue splits are not publicly disclosed by either platform.

As wrappers (like brokers and media) distribute across many rails, they will demand standardized contract specifications with comparable markets, so rails that lead this charge could be rewarded with quick integrations.

An entire ecosystem of applications, powered by this novel primitive, and it goes far beyond the minimizing “Polymarket vs. Kalshi” debate - we’re talking about dozens of killer businesses at the periphery that are about to be enabled. But most of these businesses will only work where liquidity is real and contract specs are legible.

And who will be paying for these services?

Again, it breaks down by the type of market we’re talking about and what layer of the stack is in focus:

- Cadence Markets: rail fees are funded by retail entertainment flow; wrapper economics are funded by retention loops and cross-sell.

- Narrative Markets: rail fees are funded by attention-driven trading; wrapper economics can be funded by probability-as-data distribution (publisher/institutional embeds) plus power-user tooling.

- Hedging Markets: rail fees are funded by hedgers and informed traders; wrapper economics are funded by workflow embedding (brokers/terminals) and trust/permissioning.

Of course, this is a simplification. After all, Polymarket has sports markets and Kalshi has politics and crypto, but we see these as examples of cross-selling to users, not the platforms’ main courses. You go to Kalshi to bet on the Super Bowl and realize they have midterm markets too, how convenient. It’s the same as 7-11 enticing you with BigGulps and Funyuns when you go in to get your daily scratchers, it’s just good business.

The stack explains where value can accrue. User behavior determines whether it does. If Cadence Markets are powered by high-frequency retail flow, Narrative Markets by attention + positioning, and Hedging Markets by informed hedgers, then the next question is: do the observed flows actually match those stories? Let’s look at who trades, how they trade, and what that implies about where true price discovery happens.

User behavior and onchain patterns

For prediction markets especially, who trades and how they trade matters more than in most asset classes because each individual market is really a one-off micro-asset. Trading price of the markets only becomes signal when the right cohort is in the trenches.

We’re gonna track four distinct behaviors across the sector and use it to answer some key questions:

- Participation breadth & retention: is this a one-off spike or are habits forming?

- Concentration: can we assume wisdom-of-the-crowds or is everything whale dominated?

- Trading posture: are users mostly opening simple positions or actively managing risk?

- Liquidity assumptions: are market makers helping users easily enter/exit?

The answers to these questions will clue us into the health of the sector as well as how well the leaders are optimizing for their target audience.

Participation breadth and retention (what adoption looks like)

Top-line numbers are looking great, with Polymarket breaking 300K unique returning users per week and consistently adding 30-50K new users to go along with it.

This broadening participation and improving retention tells us that prediction markets as a sector have graduated from an event-driven curiosity to a mainstay. People aren’t just checking into the markets when an election is in full swing, they are using it to check the pulse of the world (and to participate in the commotion).

Concentration and whale dominance (is “wisdom of the crowds” possible?)

For a prediction market to, well, predict, it requires a critical mass. This is real science by the way, studies have shown (Standford/UCSD study, PDF warning) that “aggregate opinions of groups are often more accurate than those of the constituent individuals.” Which is why Polymarket absolutely smoked pollsters in the 2024 election cycle.

Polymarket in particular has faced heavy scrutiny for alleged insider trading taking place on its platform and has recently partnered with the likes of Palantir and TWG to shore up its defences. Regardless, we’d like to see that it isn’t simply a few big whales making wild swings on most markets, but a wide cross-section of users from all over the world.

On Polymarket in particular, we see “whale dominance” declining, with the top 100 traders by volume going from >95% of platform volume in 2024 to 61% today. We see this as a maturity signal, reducing manipulation/narrative risk and making Polymarket’s probability-as-media roadmap much more credible.

What trading posture tells us about who uses these markets

Casual users and traders display different patterns of behavior - and we can see it in the data.

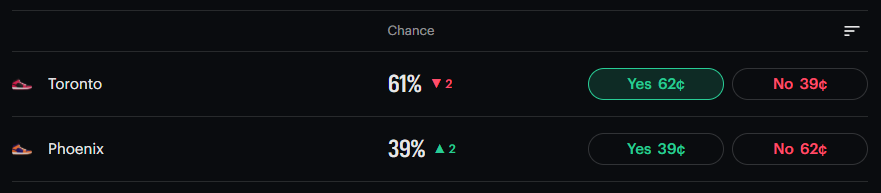

For Kalshi, we see a clear preference for traders to take the “YES” side over “NO,” especially in 2025, by a 2.49x margin.

When we remember that the majority of Kalshi volume has been in sports markets, this begins to make sense. On most of these markets, buying “Toronto YES” (as below) is economically similar to buying “Phoenix NO,” so the YES/NO split is better read as: how users choose to express the view (with the affirmative framing and UI defaults), not a directional asymmetry in economics.

Put another way, people prefer to click the positive proposition, betting on their team to win rather than on their opponent to lose.

This suggests that we’re witnessing a lot of retail activity, since you’d expect a more balanced weighting from a price-sensitive buyer (assuming better prices are distributed evenly between the YES and NO sides for a large enough pool of markets).

As far as price takers on the Polymarket side, we see that SELLs dominate the BUYs by a wide margin. This supports a “more trader-like posture” story, suggesting that a meaningful share of takers are hedging/liquidating, not only opening fresh directional bets.

This all tracks with our assumption that Cadence Markets (like Kalshi) cater to retail flow (who you could classify more on the “gambler” side) and Narrative Markets (like Polymarket) are more suited for trader activity (with participation from our Information traders, Narrative commentators, and some Hedgers).

Near-resolution dynamics and the market-maker question

Unlike traditional options markets, market makers face off in a game of chicken when it comes to holding their positions close to expiration. The binary payoffs (0 vs. 1) make inventory risk a serious concern for market makers, with small information shocks or late news meaning a complete wipe out of inventory PnL. The knee-jerk reaction to this would be to: quote smaller, widen spreads, or reduce presence altogether as the expiration draws nearer.

We observe this phenomenon in the data, with spreads and price impact actually increasing as resolution draws nearer, indicating that liquidity thins out when the end draws near.

That is our interpretation of the data, anyway. It could be argued that other forces are at play, such as a tendency for traders to size heavier into markets that are close to expiry or for traders to accept higher slippage to jam their bids in at the late stages. This would go along with the idea that platform-aligned market makers have obligations to support markets to completion. We leave it up to the reader to come to their own conclusions.

It’s important to understand the user posture because that tees up which wrappers will win (brokers vs terminals vs media), and near-resolution liquidity dynamics shape which product archetypes can scale (Cadence vs Narrative vs Hedging).

So the debate isn’t “gambling vs forecasting.” It’s whether these products can reliably convert attention into tradeable markets without breaking at the moments that matter most - near resolution, during shocks, and in thin long-tail contracts. Every major innovation we’re seeing is aimed at one of those failure points: packaging (combos), liquidity provision, distribution surfaces, and new contract formats that broaden what can be traded. Let’s look at what’s actually new.

Key innovations (what’s actually new)

This is not going to be a one-stop-shop for every new app in the prediction market space. Instead, we’re going to use this section to look for leverage points - which changes are actually capable of moving liquidity, trust, retention, and/or distribution.

What changed: Perps venues are experimenting with outcome markets as a generalized contract type, trying to absorb event risk into a perps-native stack.

Why it matters: If successful, this is the cleanest “event risk becomes a standard trading primitive” path for crypto-native traders (margining, UX, distribution already exists).

Examples:

What changed: Pressure is rising to standardize contracts (spec templates, sources, windows, and identity mapping) so distribution wrappers can safely scale and compare markets.

Why it matters: Standardization is the unlock for “multi-rail” futures: without it, cross-venue routing and best-execution-like experiences remain fragile.

Examples:

What changed: A growing “professionalization layer” is forming around the major rails: analytics terminals, alerts, and cross-venue comparison.

Why it matters: Tooling changes who participates (more active management, more two-way flow), and accelerates market reflexivity.

Examples:

What changed: Integrity policing is becoming explicit: regulated rails emphasize audit trails and enforcement; crypto rails are adding monitoring partnerships and ecosystem tooling.

Why it matters: If “information-advantaged” participation improves accuracy, integrity tooling is what prevents the whole category from being dismissed as rigged.

Examples:

What changed: New market designs aim at signal beyond binary “will it happen,” and niche communities aim to win via culture and distribution, not global liquidity.

Why it matters: These niches don’t need to beat incumbents on total volume - they need to own a distribution surface (Discord, mobile, creator channels) and a tight user cohort.

Examples:

The clean way to read this wave of innovation is as constraint-hunting: teams are trying to unlock liquidity formation (often via distribution and market-making mechanics), harden trust under stress (settlement integrity and reputational resilience), or expand what users can express with one trade.

A few innovations (especially probability-as-data) are less about changing execution and more about packaging the market’s output for distribution, but they still tie back to the same constraints by shaping where attention and legitimacy accrue. Once you map these moves onto rails and wrappers, the category starts looking like a stack that stratifies by cohort and by distribution surface. We’ll close by stating a base case and a bull case, and where we could see it all breaking down.

Our short-term outlook on prediction markets

No “state of” report would be complete without a healthy dose of peering into our crystal ball. Here’s the no-nonsense base, bull, and bear checklist items we’re watching for.

If we look out 12-24 months, here’s what we see coming:

- Cadence Markets (namely Kalshi, through their sports + combos) scale fastest through distribution wrappers, with regulated rails continuing to win broker integrations.

- Polymarket continues to dominate Narrative Markets, especially where speed-to-list and breadth matter.

- Hedging Markets start gaining traction, becoming the acceptable entry land for TradFi incumbents because standardized specs are the easiest to approve and distribute. Watch for HIP-4 as well as Nasdaq/Cboe experimentation this year.

- Even beyond Hedging Markets, we’re watching for a big structural push towards more market standardization wherever possible. As brokers distribute across rails, they will demand comparable contracts and clearer specs. We could see some movement on this from Polymarket post-token announcement.

Overall, this is a push towards maturity and role definition. People will understand that you go to Kalshi for the best sports markets, Polymarket for the highest signal & narrative markets, and Hedging Markets to hedge out hyper-specific risks in your portfolio.

If we put our bull hats on (we never took them off), we see a blossoming sector forming over the next couple of years.

- Liquidity expands beyond headline markets, where breadth deepens (not just volume), and market maker participation remains durable even near resolution.

- “Probability-as-data” becomes a meaningful parallel business line, allowing the dominant player(s) to monetize even when users don’t trade.

- Disputes remain rare relative to market count, with dispute rates falling as scale increases - necessary for trust.

As always, we have to ask - “but what if we’re wrong? What would that look like?”

Not sure if you’ve noticed, but not everyone is as excited about prediction markets as we are. So here’s what the bear case would look like:

- Category-level backlash concentrates around integrity and “information hazard” markets (e.g. war, assassination, death), and platforms are forced into a narrow scope & liquidity collapses into a small set of “safe” markets.

- Concerns over insider trading push platforms to over-regulate, investigate not just insider trading but traders with legitimate edge (“sharps”), scaring away the user base most likely to nudge markets towards reality and provide meaningful signal.

- Long-tail economics worsen: the power law tightens (volume concentrates to just a few markets), and mid- and long-tail markets become effectively untradeable.

- Without chronic market maker support, what we see with near-cycle resolution only worsens, with traders unable to exit close to market expiration.

We’re past the point of wondering if prediction markets will meaningfully penetrate the global zeitgeist. Whether you consume the majority of your content through Twitter, YouTube, or mainstream media, this infrastructure has found its way into the conversation.

The question now shifts from “does this have legs?” into “who will capture meaningful market share?”

Our argument has been that the key to sussing out the victors will come down to:

- Who can win the rails for each market archetype and

- Who can wrap their product to best hunt the constraints of: liquidity formation, trust, or expressiveness

The end-state will not be a single winner, more likely it will look like a stratified stack across Narrative Markets, Cadence Markets, and Hedging Markets, each bundled differently across rails and wrappers.

In closing

The data suggests the category has crossed the threshold into infrastructure - but it’s still asymmetrical: execution quality and market breadth don’t scale evenly across rails.

That’s why this is a stack war: rails compete on settlement credibility and depth, while wrappers compete on distribution, retention, and packaging. Narrative Markets, Cadence Markets, and Hedging Markets are simply different equilibrium bundles of those layers, optimized for different user intents. The durable advantage goes to whoever can standardize enough to scale distribution without losing the permissionless edge that keeps markets culturally relevant.

Where does each player stand today? Here’s how we see it:

A snapshot of competitive positioning across the key dimensions that matter. Hover over any cell for rationale. ● = strong today ● = mixed / developing ● = weak / not live ● = N/A

| Player | Liquidity (Top) | Liquidity (Breadth) | Distribution Power | Settlement Credibility | Data / Prob. Brand | Institutional Readiness |

|---|---|---|---|---|---|---|

| Polymarket | ● | ● | ● | ● | ● | ● |

| Kalshi | ● | ● | ● | ● | ● | ● |

| CME | ● | ● | ● | ● | ● | ● |

| Nasdaq | ● | ● | ● | ● | ● | ● |

| Cboe | ● | ● | ● | ● | ● | ● |

| Coinbase (wrapper) | ● | ● | ● | ● | ● | ● |

| Robinhood (wrapper) | ● | ● | ● | ● | ● | ● |

Nasdaq and Cboe liquidity is ● because their prediction-style products are not live at scale today, even though their settlement/institutional infrastructure is strong. Coinbase and Robinhood liquidity is N/A because they are wrappers - their score reflects distribution and permissioning posture, not where the order book sits.